2022-23 Budget – Tax Measures

time:2022-02-28

In his 2022-23 Budget, the Financial Secretary proposed the following measures:

The Financial Secretary proposed a one-off reduction of profits tax, salaries tax and tax under personal assessment for the year of assessment 2021/22 by 100%, subject to a ceiling of $10,000 per case. This measure will be effected by amending the Inland Revenue Ordinance.

For profits tax, the ceiling of the tax reduction is applied to each business. For salaries tax, the ceiling is applied to each individual taxpayer; but for married couples jointly assessed, the ceiling is applied to each married couple (i.e. capped at $10,000 in total). For personal assessment, the ceiling is applied to each single taxpayer or married person who elects for personal assessment separately from his/her spouse. If a taxpayer elects for personal assessment jointly with his/her spouse, the tax reduction is capped at $10,000 for the married couple.

The proposed tax reduction is not applicable to property tax. Individuals with rental income, if eligible for personal assessment, may be able to enjoy such reduction under personal assessment.

A taxpayer who is separately chargeable to salaries tax and profits tax can enjoy tax reduction under each of the tax types. For a taxpayer having business profits or rental income and electing for personal assessment, the reduction will be based on the tax payable under personal assessment. It might be different from the amount of tax reduction he/she would get if he/she was not assessed under personal assessment. The exact position will need to be evaluated case by case.

To elect for personal assessment, eligible taxpayers should complete Part 7 of his/her tax return for individuals (BIR60) for the year of assessment 2021/22. Individuals having salaries income only, but no business profits and rental income, need not elect for personal assessment.

The proposed reduction will reduce taxpayers’ amount of tax payable for the year of assessment 2021/22. Taxpayers should file their profits tax returns and tax returns for individuals for the year of assessment 2021/22 as usual. Upon enactment of the relevant legislation, the Inland Revenue Department will effect the reduction in the final assessment. For any final assessment for 2021/22 issued before the enactment of the law, the Inland Revenue Department will make a reassessment after the enactment. Taxpayers are not required to make any applications or enquiries to the Department.

The proposed tax reduction will only be applicable to the final tax for the year of assessment 2021/22, but not to the provisional tax of the same year. Therefore, taxpayers are still required to pay their provisional tax on time despite the proposed reduction measure. The provisional tax paid will be applied to pay the final tax for the year of assessment 2021/22 and the provisional tax for the year of assessment 2022/23. Excess balance, if any, will be refunded.

Waiving business registration fees for 2022-23

The Financial Secretary proposed to waive business registration fees for the year 2022-23.

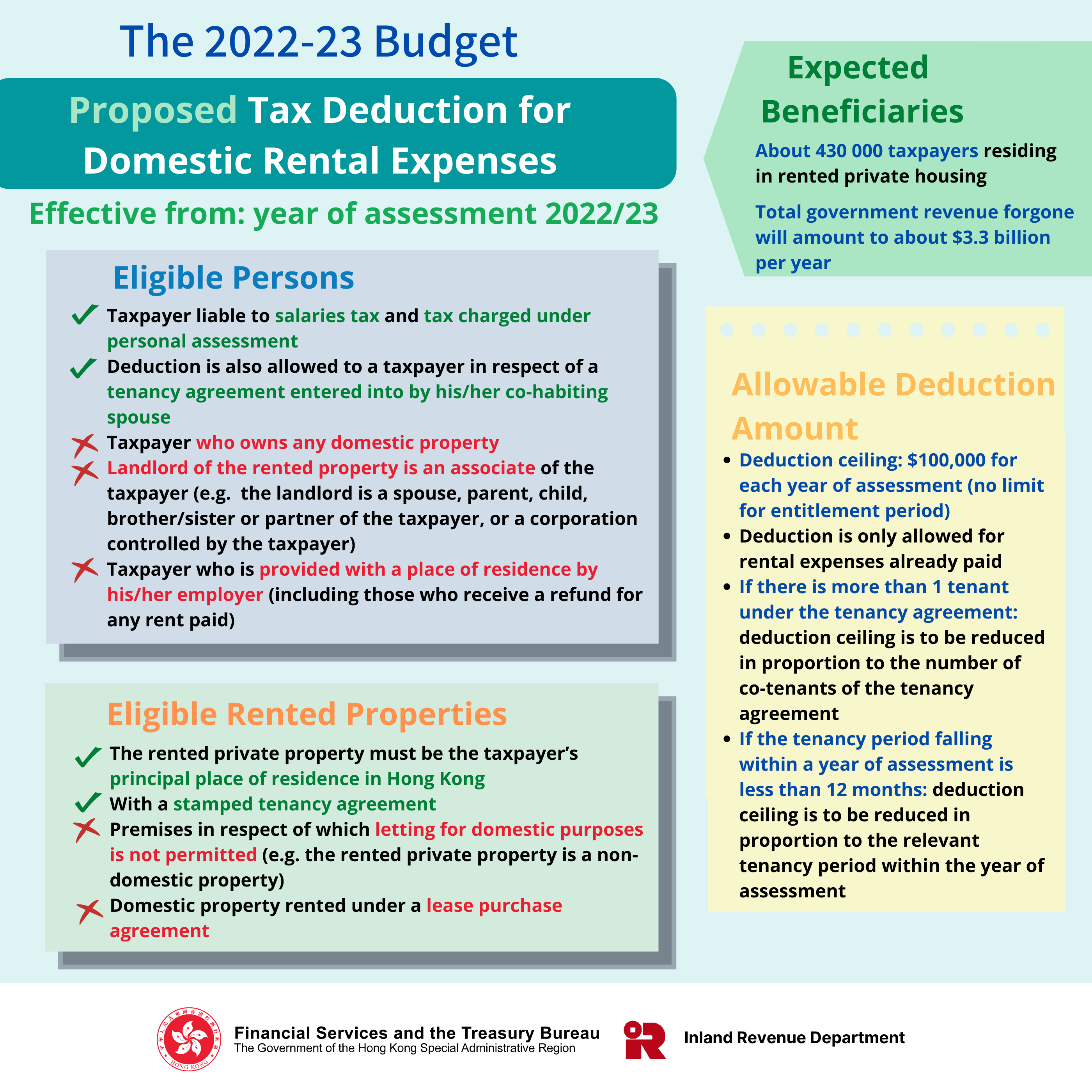

Introducing a tax deduction for domestic rental expenses

The Financial Secretary proposed to introduce a tax deduction for eligible domestic rental expenses from the year of assessment 2022/23. Taxpayers liable to salaries tax or tax charged under personal assessment who do not own any domestic property can claim deduction for the rent paid by him/her or his/her spouse as the tenant. The annual ceiling of the deduction is $100,000.

All the above measures can only be implemented after completion of the relevant legislative process. It should be stressed that details of the measures are subject to change during the legislative process.